Lessons learnt on unconditional cash transfers in Haiti

- Issue 54 New learning in cash transfer programming

- 1 Bigger, better, faster: achieving scale in emergency cash transfer programmes

- 2 'More than just another tool': a report on the Copenhagen Cash and Risk Conference

- 3 Cash transfers and response analysis in humanitarian crises

- 4 A deadly delay: risk aversion and cash in the 2011 Somalia famine

- 5 Institutionalising cash transfer programming

- 6 New technologies in cash transfer programming and humanitarian assistance

- 7 Innovation in emergencies: the launch of 'mobile money' in Haiti

- 8 Lessons learnt on unconditional cash transfers in Haiti

- 9 Fresh food vouchers: findings of a meta-evaluation of five fresh food voucher programmes

- 10 Bridging the gap between policy and practice: the European Consensus on Humanitarian Aid and Humanitarian Principles

- 11 Humanitarian financing and older people

- 12 The rehabilitation response in Haiti: a systems evaluation approach

- 13 Working with Somali diaspora organisations in the UK

- 14 Applying conflict-sensitive methodologies in rapid-onset emergencies

The challenges of responding to the catastrophic earthquake in Haiti in January 2010 were huge and varied, prompting agencies to think and act creatively. Christian Aids partners distributed cash to people affected by the disaster two weeks after the earthquake struck. Some Christian Aid partners chose to respond with cash, rather than with goods in-kind, as they recognised the diverse needs of those affected, the flexibility of cash to meet those needs, the importance of preserving peoples dignity by transferring choice to them and the need to support local markets.

The cash response

Initial assessments highlighted the enormous range of needs, including food and non-food items (fuel, cooking equipment, business supplies), basic services (shelter materials, payment of medical or education bills) and costs linked to displacement and reintegration (transport, rent). International agencies faced huge logistical difficulties in sourcing and distributing basic items, due to transport, storage and infrastructural damage, making cash a more cost-effective option than providing goods in-kind. As local markets began to function just a few days after the earthquake, cash transfers were an efficient and effective response. Cash transfers also reduced the need for people to take out further loans to compensate for loss of incomes and livelihoods.

The primary aim of the cash transfers was to meet basic needs. The size of the transfer was calculated according to the market value of a Sphere standard dry food ration basket. The value was set at $26 per person per month. With an average family size of five, $130 was proposed as a monthly household cash value for distribution. Four of the six Christian Aid partners that responded immediately elected to use unconditional cash transfers, though each designed their programme differently:

- Partner 1 distributed $52 once in rural and peri-urban settings to IDPs and host families.

- Partner 2 distributed $26 three times ($78) in rural areas, also to IDPs and host families.

- Partner 3 distributed $390 once in urban and peri-urban areas to people living with HIV/Aids.

- Partner 4 distributed $130 three times ($390) to IDPs in peri-urban camps.

Distribution mechanisms

1. Remittance agents

Partner 4 set up a contract with a remittance agent, Caribbean Air Mail (CAM), a well-established agency used to sending funds from the US, Canada and the Dominican Republic to recipients in Haiti. In 2009 remittances into Haiti totalled 15.4% of GDP; see http://siteresources.worldbank.org/INTLAC/Resources/Factbook2011-Ebook.pdf. CAM was the only surviving remittance agent in the peri-urban camp where Partner 4 was working. Under the contract CAM was to transfer cash to a predetermined list of beneficiaries, compiled by the partner agency based on early assessments. Beneficiaries were given ID cards with unique issue numbers and distribution punch holes. This information was passed on to CAM, which then batched the distributions into groups with specific date and time slots for collection. CAM was responsible for preparing the money, recording receipts and making security arrangements, and it charged the partner a 3% fee for these services. The partner was responsible for informing the beneficiaries of the distribution days and times, observing the distributions and addressing any issues raised during the process. The first transfers were made 14 days after the earthquake, and beneficiaries were treated in the same way as existing CAM customers, giving them a sense of dignity and removing the impression of being part of an aid distribution.

2. Cash envelopes

Three of the partners used direct distributions with cash envelopes, alongside complementary distributions of food and shelter materials and psychosocial and health activities. This approach was efficient in the first few weeks after the emergency, as the banking system was not fully functioning, the number of households to which funds were to be distributed was relatively small (a maximum of 2,000 families per partner) and it was suitable for community sites with a wide geographical spread. The partners controlled the distribution, communicating the date, time and location, or distributing directly to each home. ID cards were made and record sheets kept. Direct distribution avoided the contract fees levied on Partner 4 but involved a higher human resource cost, reducing the amount of funds directly reaching beneficiaries. However, Partner 4s beneficiaries had to wait longer at distribution points than they did with direct transfers. Three-quarters of beneficiaries queued for more than three hours to collect funds from CAM, compared to 13%17% waiting three hours or more for the cash envelope distribution.

Impact

Spending patterns

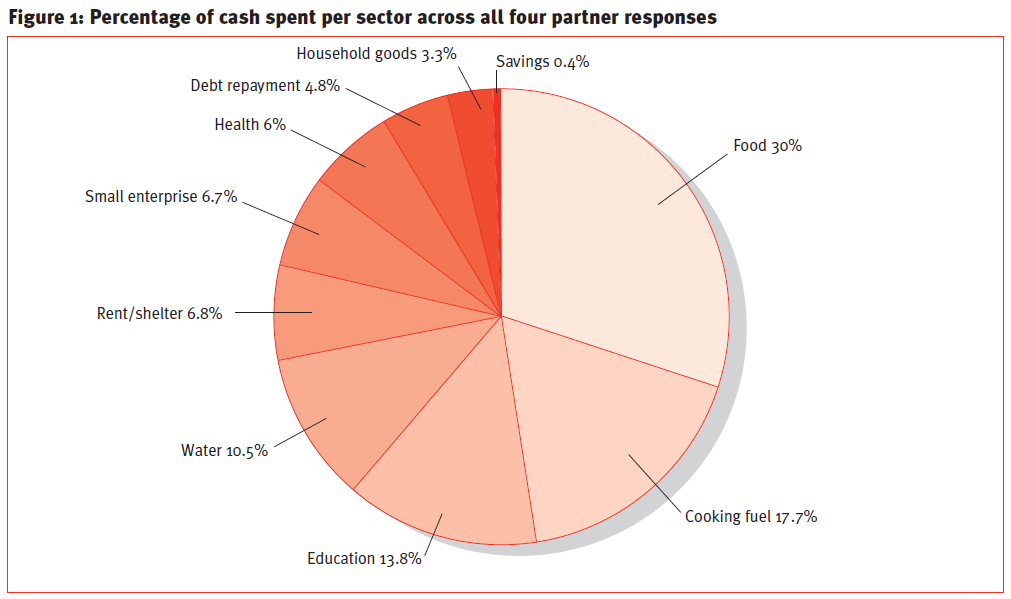

Figure 1 illustrates the wide range of things beneficiaries did with the cash they received. A more traditional in-kind response could not have met such a diverse range of priorities.

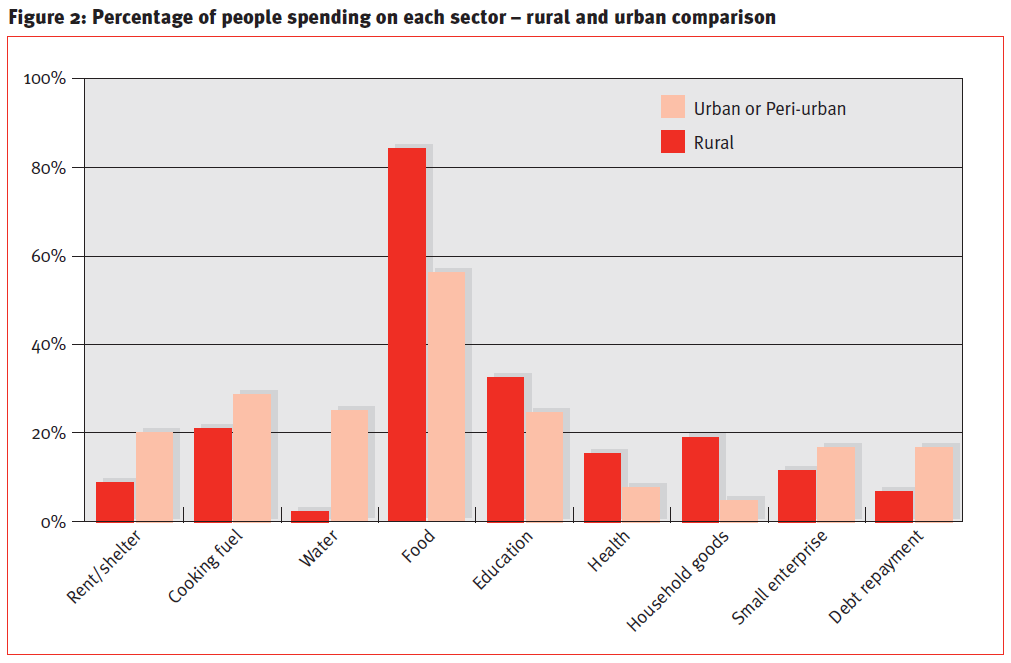

By comparing how cash was used in rural and urban/peri-urban areas (Figure 2), the versatility of cash becomes clear. People in urban locations had greater shelter, fuel, water, debt and small business needs, whereas in rural areas 28% more people prioritised food.

While the cash transfers were targeted at households rather than individuals, it was important to assess whether the gender of the cash recipient greatly affected the spending decisions. The evaluation data revealed almost no discernable difference, with the greatest variation being that women were slightly more likely than men to purchase cooking fuel (3%) and food (2%), while men were 2% more likely to use the cash to pay for education and health costs than women.

Debt and credit

An average of 5% of all the cash distributed by Christian Aids four partners was used to repay existing debts, and 15% went on replacing lost household goods and small-business items, allowing some families to recover and generate income without needing to take on further debt. Despite this, roughly 33% of the programmes beneficiaries accessed additional sources of credit. Nationally, 13% more Haitian households were in debt in 2011 than before the earthquake, with rural indebtedness higher than urban. See www.acted.org/en/haitianhouseholds-economic-situationand-indebtedness. Had more agencies responded with cash transfer programming targeted at rural households, hosting families and the displaced, this trend might have been reduced.

Savings and investment

One partners decision to disburse a large, regular transfer of $130 a month for three months ($390 in total) created the best chance for beneficiaries to start or restart a business, compared with a single transfer of the same cumulative amount of $390. Less than 2% of those receiving a single transfer were able to make any savings, whereas those with two or more transfers were 24% more likely to do so, regardless of the cash value given, so in this case the cash value is less significant than the number of transfers received. This illustrates that well-planned cash transfers can meet basic needs and give individuals control and decision-making power over their own recovery.

Beneficiary satisfaction

The evaluation found that 98% of a sample of 166 beneficiaries preferred cash transfers over in-kind distributions and while there are often security concerns when designing cash transfer programmes, the data gathered showed that 94% of beneficiaries did not share this concern during the distributions. This is significant since 58% of beneficiaries were living in camps or tents set up within cities, and had limited control over their own security. An overwhelming 66% agreed that a regular monthly transfer was the preferred frequency, followed by 17% who favoured once a week. It is clear that the one-off payment of $52 made by Partner 1 was seen as deeply unsatisfactory, while Partner 2 gave only $26 more ($78), but spread over three transfers, resulting in a much greater degree of satisfaction. One explanation is that Partner 2 worked in rural locations, where the base income was significantly lower than in urban or peri-urban locations, leading to greater appreciation of the cash transfer.

Lessons from the cash response in Haiti

Working through local partners with existing contacts and relationships almost certainly speeded up the delivery of the cash transfers. Using the existing remittance system avoided delays and allowed beneficiaries to access funds through a familiar system. While cash envelopes were reasonably fast and cost-effective, they required additional security measures. The use of unconditional cash led to a number of unexpected outcomes, with some funds used to start or restart a business, repay debt and even save. Beneficiary consultation and awareness-raising in advance meant that almost all households had no security concerns. Christian Aid and partners were more worried about security than beneficiaries. The Cash Working Group, which was set up very early on, was an excellent way of building momentum and increasing agency confidence, and created a community for sharing and producing monitoring and evaluation tools. In an external evaluation, the partner distributing a cash-only response, as opposed to cash and other activities, was found to have the greatest impact and was the most efficient.

Preparedness is fundamental but is often overlooked. Much can and should be done in advance setting up contracts for vouchers, mobile cash, remittance and banking networks to broaden the possible response options. In this example the amount of the cash transfer was less significant to the beneficiaries than the number and frequency of transfers, with regular transfers allowing beneficiaries to save some of the cash they received. The preferred frequency would have been one transfer a month. Using existing systems such as remittance agencies has enormous benefits in terms of speed of set-up, familiarity and lack of stigmatisation. However, this system can create delays and long queuing times if not well-designed. A clear and well-communicated distribution schedule, distances from homes to collection points and the provision of seats and shade for more vulnerable people should be considered, as per other distribution plans. Agencies need to consider debt implications if responding with in-kind or conditional cash. The experience and lessons learnt from cash programming will inform Christian Aids future work in Haiti and beyond.

Kate Ferguson was formerly Haiti Emergency Programme Officer at Christian Aid. This article is based on a Christian Aid Humanitarian Briefing Paper entitled Haiti: Unconditional Cash Transfers Lessons Learnt, published in January 2012.

Comments

Comments are available for logged in members only.